Tokyo land is still >$85 million an acre

What will happen to the highest-priced metro housing markets after YIMBYs achieve realistic housing abundance?

Megacity YIMBYism lowers rents but not land values—plus who wins, who loses, and why most mortgage-holders shouldn’t worry.

When you zoom out on American politics, one pattern that snaps into focus is how much local elected officials focus on preserving, even boosting, home values. It’s a reasonable political instinct. Roughly two-thirds of American adults live in owner-occupied housing, and for most of them the home is by far their largest asset. The threat that finally building enough housing to satisfy pent-up demand would crash widely-held asset values is taken seriously across the spectrum—by populists who promise rising prices to homeowners, by mortgage-market watchers who remember 2008, and by political-economy theorists in the William Fischel tradition who treat homeowner profit as the prime mover of American zoning.

That fear is mostly wrong, but in an interesting way. Good public policy should indeed raise total land values: insofar as land markets are efficient at capturing all the “goods” and “bads” about living in a particular location, policymakers and society at large should want high land prices because they proxy for good wages and high quality of life.

Thus the right question isn’t whether YIMBYism would lower the user cost of housing—that’s the whole point of the YIMBY movement and the unanimous upshot of the academic urban economics literature—but whether it would lower the value of land overall. The answer will almost certainly turn out to be no, because higher land prices are substantially severable from, and can coincide with, lower structure prices. And Tokyo, the world’s largest city and the only one that features anything like a realistic best-case version of housing abundance at megacity scale, is the cleanest place to see it.

The world’s largest YIMBY metropolis still has more than $85M-an-acre dirt

Tokyo is the world’s largest single metropolitan labor market. Greater Tokyo holds about 37M people, and it’s still growing as Japan’s countryside empties out and reforests. As a comparison, Tokyo first surpassed NYC in population in the early 1960s; after decades of steady growth, its nearly twice the size of metropolitan NYC’s 19.3M residents.

By the standards of Anglosphere megacities—New York, London, Toronto, LA—Tokyo housing is famously cheap. Builders can put up small-lot single-family homes, midrises, microapartments, and single room occupancy-style shared housing units with ease and in large volumes. (High-rises are not allowed by-right everywhere, so this isn’t a pure laissez-faire experiment, just the closest real-world example.) If “Tokyo regulation” is what real-world YIMBY victory looks like in a global megacity, it’s the best dataset we have.

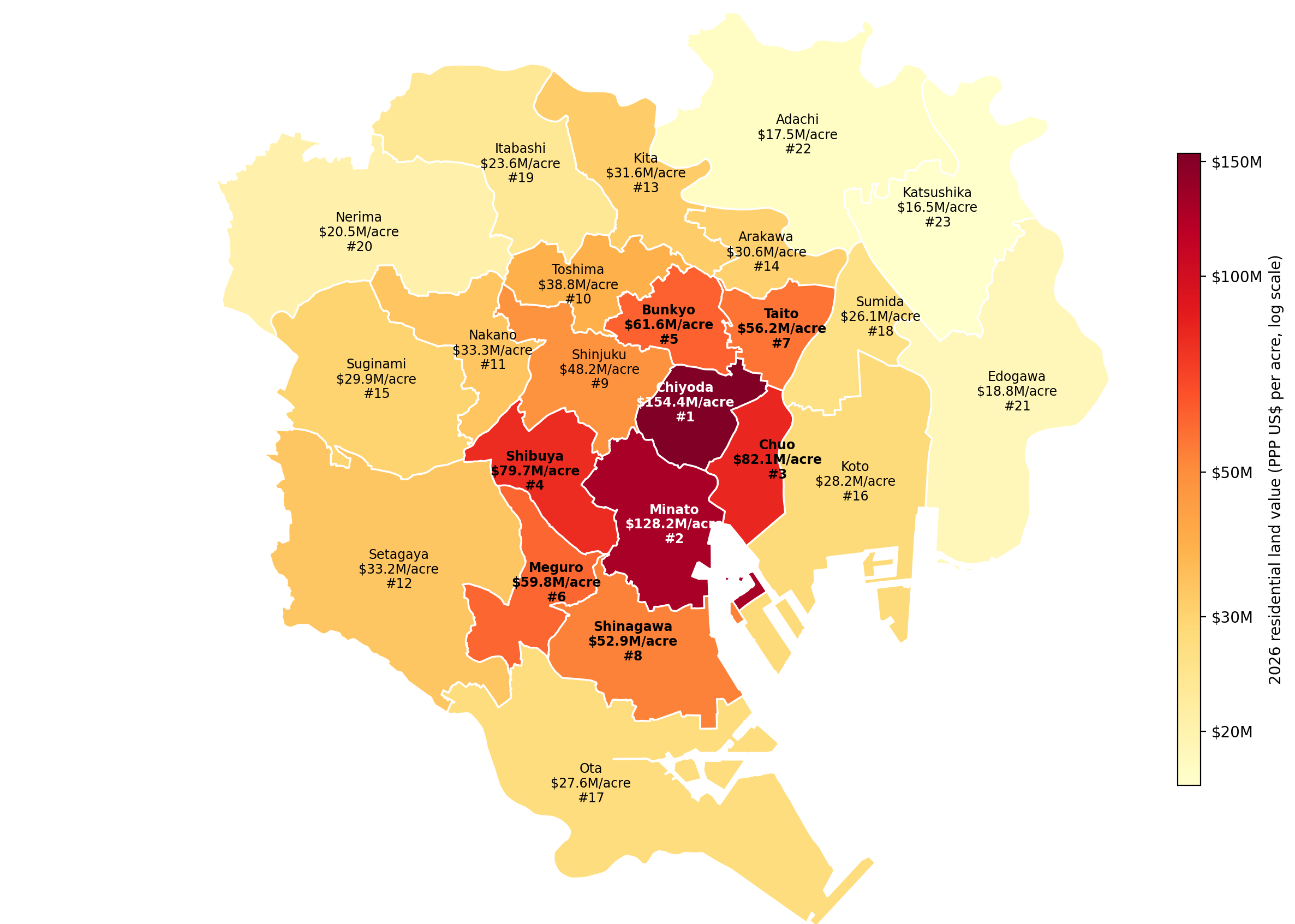

So what are Tokyo’s land prices?

Prices for land range from well over $100M per acre in the urban core (in 2024 USD, PPP-adjusted) to just under $20M per acre on the periphery of Tokyo proper’s 23 wards. Whether one uses PPP (~$154M/acre) or market conversion rates (~$90M/acre) is not particularly important to the thesis: The point is that land prices are extremely high, and demonstrate a typical metropolitan bid-rent gradient from the core to the periphery.1

The famous (relative) cheapness of Tokyo housing is not a story about cheap land. A one-acre detached house in central Tokyo would cost more than $100 million in dirt before you broke ground. The land is pricey but the structures are cheap. Admittedly, Tokyo’s rents and prices are not as cheap per square foot as buildings in the US Sunbelt’s midsize cities, but cheap by the standards of any 10-million-plus Anglosphere metro area. Tokyo built its way to relative affordability without ending up with low land values, and the values themselves look reasonable for a productive, agglomerated megacity that simply didn’t artificially restrict its own supply.

Land prices and structure prices are related but different things

Standard urban economics tells us that wages and amenities accessible from a location capitalize into the price of land at that location. The harder practical upshot, which Ed Glaeser and his coauthors have spent their careers teaching, is that whether high land prices translate into high structure prices is a function of land-use regulation.

High land prices are a price signal. They tell builders to economize on land per unit by stacking up more structure—more floors, smaller footprints, higher floor area ratios per unit of land. In a liberally regulated environment, the bid-rent gradient for land can be extremely steep, while the bid-rent gradient for structures is much shallower.2 Structure costs do rise with height—the U.S. model building code introduces real cost steps as a structure grows in density. A build starts needing tuned mass dampers and bespoke engineering somewhere past 50 stories—but those increases should be shallower than the underlying land-price gradient if regulation allows.3

As a useful sanity check on what land prices are really capitalizing: Consider tightly zoned waterfront cities, where the going price (and waitlist) for houseboat moorings—physically not land at all—behaves like part of the residential property market. The product being priced is not actually dirt! It’s locational access to the bundle of public and private goods available at that point on the map. Upzoning lets builders amortize that location access cost over more buildable square feet. It does not, and could not, reduce the value of the access itself as long as the net external congestion costs of growth don’t exceed the net external amenity and wage-agglomeration benefits of growth.

When policymakers upzone widely with by-right permitting across a high-demand metro, two things should happen at once. Measured per-acre (like farmland), land value rises, because the parcel has been granted a valuable option to host more buildable area. Land value measured like NYC-area developable land per buildable square foot falls, because that higher per-acre value is being amortized over much more floor area.

These move in opposite directions, and neither one alone is “the land price” in the sense political conversation usually means. This distinction dissolves a lot of the political-economy panic around housing abundance. Again, land prices quoted the way NYC land brokers quote them, on a “Zoning Square Feet” or “Buildable Square Feet” basis, will fall even as the total value of land is at least stable or rises in the metro area being upzoned.

The Homevoter Hypothesis Can’t Explain Everything

The leading academic framework for explaining American NIMBYism is Dartmouth economist Bill Fischel’s pairing of fiscal zoning and the homevoter hypothesis.

The fiscal-zoning argument is that single-family-only zoning and large minimum lot sizes are profit maximizing tools for managing the local tax base: By excluding apartments and small houses, exclusive suburbs effectively “faregate” the municipal border, restricting admission to households whose property taxes will exceed their consumption of local public services like schools. Local public goods become club goods, and the club charges admission at the municipal border rather than the schoolhouse door. Instead of hosting private for-profit schools, these suburbs act as private for-profit neighborhoods with an ostensibly “public” school inside.4

The homevoter hypothesis is the political mechanism: Homeowners turn out in local elections to defend the asset values that this fiscal arrangement protects.

Fischel’s homevoter hypothesis rests on two claims: that single-family zoning maximizes the asset value of incumbent owners, and that those owners (the electorally pivotal median voter in most US jurisdictions) turn out to defend it.5 The second half holds up in the suburban cases Fischel built the theory around. The first half breaks in the cases that matter most for national productivity: the high-demand cores of America’s largest cities.

Tokyo’s land and property market conditions show why: Tokyo combines metropolitan housing abundance with land prices that remain high, not low. The two facts coexist because the relevant scarcity isn’t housing supply; it’s centrally-located land. A homeowner sitting on a single-family parcel in a high-demand Tokyo ward holds a portfolio that is overwhelmingly land. Upzoning her parcel raises the value of that land, sometimes dramatically, because the parcel can now carry dozens of units rather than one. The option to redevelop is worth more than the right to preserve neighborhood character. Restrictive zoning, in this regime, is asset-destructive for a land-rich homeowner in a high-demand area.6

If American single-family homeowners in the cores and first-ring suburbs of New York, San Francisco, Boston, or LA were maximizing the dollar-denominated asset values Fischel says they care about, they would be voting to become like Tokyo landowners — to unlock the redevelopment option on their parcels. They are not. Whatever they’re maximizing, it isn’t profit.7 (See Agenda for Abundant Housing for a full-length argument.)

That’s not a fatal blow to the homevoter framework if we’re willing to relax the “objective function” of voters from strictly defined profit-maximization. As any good undergraduate economics professor will remind a student who discovers people valuing non-pecuniary interests: “Firms maximize profit. People maximize utility.” This is of course the beginning, not the end, of the question: It is the task of the other social sciences and humanities to help economists figure out what it is that people see as utility-maximizing or otherwise in their best all-things-considered interests, when consumers are not behaving in a way that maximizes apparent pocketbook dollars and cents.

Amenity preferences, socioeconomic and positional status concerns, and outright economic confusion all seem relevant — Clayton Nall and co-authors find that a slight majority of Americans believe new supply raises prices.8 But it does mean the rational-asset-defense story isn’t sufficient for the high-demand core cases…which is to say, for the cases where land-use reform would do the most national good. Maximizing “Baby Boomer suburb aesthetics” in neighborhood character is, in the cores of the most important metropolitan labor markets, a goal in direct tension with homeowner profit maximization–and all Americans, homeowner and renter alike, are collectively paying a tremendous price.

The bottom line

Tokyo is the closest thing we have to a real-world YIMBY megacity, and Tokyo land is still very expensive. Tokyo builds at a Sunbelt city pace–around 2% per year–far higher than other global megacities. Cheap housing and expensive land are the very likely fruits of successful housing abundance in America’s superstar cities, and also in most of the desirable areas of our other cities.

Aggregate land values should rise with wage and amenity access under abundance, even as the geographic distribution of land values will change. Per-unit prices will fall. Land-rich owners will profit. Structure-rich owners will likely take a haircut. All renters win. And, importantly, the mortgage market will not break provided we don’t time a supply rollout to coincide with a recession.

Finally, the political-economy theory that homeowner asset defense explains American zoning has to reckon with the fact that, as Tokyo’s high post-Abundance land values indicate, the assets in question would be uplifted, not bankrupted. The narrow profit-maximizing excuse for NIMBYism does not apply to the homeowners with strong redevelopment options in the metro areas where YIMBYism can do the most good.

One could ideally just use the land price heatmap in JPY per square meter, but that’s not intuitive for a US audience. Don’t get distracted by the minutiae: All one needs to understand here is that land in central Tokyo is extremely expensive.

In the first “spatial equilibrium” model taught to urban economics undergraduates, the Alonso-Mills-Muth model, housing costs and transportation costs are simultaneously determined: Next to the central business district, commuting costs are low and willingness to pay for land is high. Far from the CBD, commuting costs are high and willingness to pay for land is low. This is called the “bid-rent gradient” or bid-rent curve. But transportation is not the only amenity or the only cost: More sophisticated models add other hedonic amenities like parks, school quality, different transport technologies, and the like. Amenities like a park can have their own local bid-rent gradient, with people willing to pay more to be closer to the park. Cities with excellent mass transit often feature bid-rent gradients around rail stations. Even privately provided public goods can generate a small bid-rent gradient if they generate enough uncaptured consumer surplus for residents in its catchment area–like a Trader Joe’s grocery store or other amenity retail.

Now, actually collecting the Japanese-language rental and sale market data to calibrate a model of the bid-rent surface of the Tokyo Metropolitan area’s market for structures, applying hedonic controls and building a repeat-transaction index, and then comparing the structure gradient to the land gradient…this would be a serious academic endeavor, not a blog post. I only have good English-language land price data at hand from the MLIT; I don’t know where to find academic-grade rental market data. But I asked ChatGPT to give it a try. Though you should treat this as synthetic demonstration data, not real fact, ChatGPT found the land gradient runs about 9× from Katsushika to Chiyoda. The asking-rent gradient runs roughly 3-4×, from around $1.10/sf/month in the cheapest wards to $3-5/sf/month in Minato and Chiyoda. If this AI-generated thought experiment based on whatever data ChatGPT found were true, the structure rent gradient would be about 3x shallower than the land value gradient.

In suburbs where the existing average wealth & incomes are high, and the marginal resident's wealth and income is lower, fiscal zoning can make parochial sense (think Woodside/Atherton, CA or Scarsdale/Rye, NY, or the Connecticut Gold Coast suburbs, etc). But if the marginal resident's income and wealth is higher than the incumbent average, then restrictions don't make fiscal sense! The persistence of growth controls blocking fiscally-positive growth in many, many US municipalities is a profound challenge to this narrowly rationalist account of growth control, even though Fiscal Zoning does help explain the behavior of the richest and fanciest suburbs that are ultimately little more than “heavily armed school districts”. Worse still: in a sufficiently politically fragmented metropolitan labor market area, no one small jurisdiction can ever unilaterally permit enough housing to meet the whole region’s housing demand, leaving individual jurisdictions in a regulatory prisoner’s dilemma with neighboring municipalities-and turning to a fraught hope that other parts of the region will continue to allow growth instead.

Fischel’s framing has well-known limits in his own telling — he’s clearest that the theory describes suburbs more than central cities, and that NYC, with two-thirds renters and a century of rent control, is a genuine exception (Fischel 2016). For our purposes the question is whether the profit-maximization premise survives in the high-demand cores where it most needs to hold.

The Squamish Nation’s Senakw development in Vancouver is the cleanest single-neighborhood demonstration. After the Canadian government returned 10 acres of urban land to the tribe, tribal sovereignty placed the parcel outside municipal planning authority. The tribe is now building a supertall residential development that will house its members and generate billions of dollars in rental income — unlocking latent land value that municipal zoning had suppressed for decades. The single-family neighborhoods surrounding Senakw could, in principle, form an exploratory committee to discover how they too might become collective billionaires. They have not. The historical analogue is Greece’s postwar antiparochi system, which replaced low-rise Athens stock with mid-rises by giving incumbent owners equity stakes in the new buildings — land-rich owners got rich, renters and first-time buyers got affordable units, and per-unit prices stayed moderate even as total housing supply expanded.

The incidence of land value uplift from regulatory reform across homeowners should not be uniform, and should vary with the newly available redevelopment options. A homeowner who already lives in a 30-story condo in central Tokyo is structure-rich, not land-rich: her unit sits on a tiny pro-rata share of land, and region-wide upzoning brings competing supply onto the market without unlocking any redevelopment option for her. Peripheral landowners face a related exposure — their land’s value depends partly on people being priced out of the more desirable core, and reform of the core erodes that exclusion premium. The rational-NIMBY coalition predicted by the incidence math is therefore narrower than Fischel suggests: peripheral landowners plus incumbent high-rise owners. The natural YIMBY coalition is renters plus centrally-located non-highrise landowners — especially single-family owners holding the most attractive developable sites. The dominant material axis is not owners-versus-renters but owners-with-development-options versus owners-without.

Folk-economic error on that scale is hard to absorb into a rational-asset-defense framework: a substantial fraction of NIMBY voting isn’t asset defense at all. It happens to coincide with the asset-defense story for some homeowners and contradicts the interests of others. This also helps explain a parallel empirical puzzle the framework struggles with — the persistence of “left NIMBY-homeowner alliances” between progressive renters and change-averse homeowners in Democratic-supermajority coastal cities, most prominently in California. Renters are the group with the most unambiguous interest in supply expansion; that they vote against it suggests some mix of confusion and willingness to incur costs for neighborhood-character preservation that the rational-self-interest framework can’t accommodate.

If only there was a way to set things up so that all that valuable land was made into the best it could be, making lots of money, and then regular bits of that money were used to fund government services....imagine if that same set up also made buying and holding pricey.....